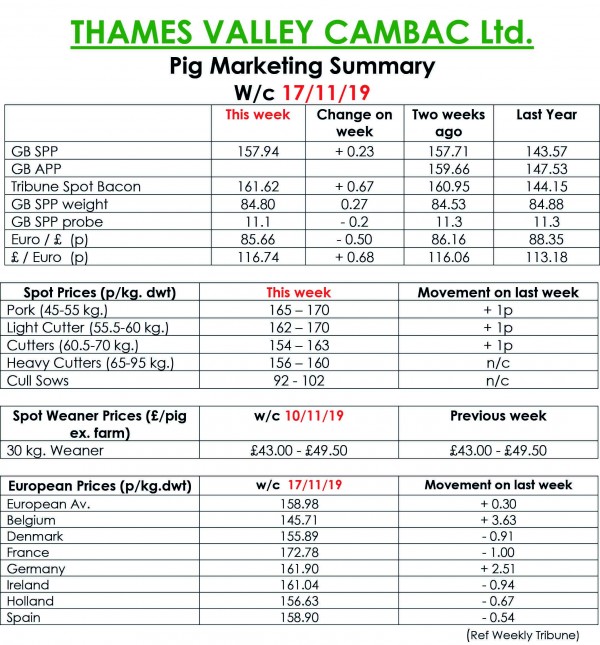

This week’s Slaughter Pig Marketing Summary, from Thames Valley Cambac, reported that the market saw little improvement this week, with most of the large processors standing on with their contract price contributions.

Mirroring last week, there were complaints of poor retail demand and slack sales, but planned Saturday kills still happened! – likely trying to secure product to service the growing export market.

TVC said the industry must find a way to tap into this new revenue stream and see at least some of the benefit percolate back down the chain to the producer. Supply remained tight and average weights were similar, but starting to track below last year.

The fresh meat market was pretty buoyant with dearer imports helping to open new trade for home produced pork. Cull sows saw a good increase, up 3p, on the back of improved continental markets. In Europe, Germany saw its first rise in nine weeks, up four euro cents, but that rise was eclipsed by Belgium up 5.2 euro cents. Price quotes in sterling were tempered however by a weaker Euro that ended the week down 50p at 85.66p.

Finally, ASF continues to spread westwards in Europe with a 300km jump in Poland after the discovery of an infected wild boar only 85km away from the German border.

The Weaner Marketing Summary, for week commencing November 10, reported that demand remained very ordinary for any supplies outside a contract arrangement. The prices announced by the AHDB saw the weighted average for a 30kg store pig fall by £2.15 to £54.87, and the weighted average for a 7kg weaner fall by 38p to £40.48p.