This week’s Slaughter Pig Marketing Summary, from Thames Valley Cambac, reported that factory reliability tried the patience of many – boilers, power supply – the list goes on.

However, producers and hauliers mucked in to keep the roll into this trading week to a minimum. Supply remained on the tight side with only the odd producer coming into the New Year with heavy weights.

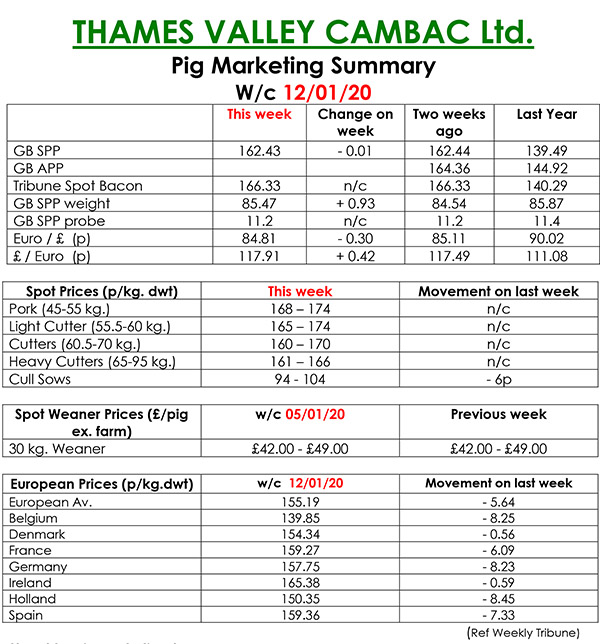

Demand was steady from a couple of the majors, but the remaining plants manged to gather up the slack. All contract prices stood on, with the SPP all but the same at 0.01p down – again quoted from a smaller sample than normal. The fresh meat market was quiet – not surprising for this time of year, but prices stood on. The cull sow market saw the biggest movement of the day, down 5p to 6p on the back of a weaker German market.

The close proximity of ASF caused farms near the German/Polish border to sell pigs early causing an oversupply. Prices were nine euro cents lower, with similar falls recorded in its near neighbours. Only Denmark and Ireland resisted this trend. Prices quotes in sterling were compromised further by a weaker Euro that ended the week down 0.30p at 84.81p.

The weaner Marketing Summary, for week commencing January 5, reported that supply of both 7kgs weaners and 30kgs store pigs tightened again with production issues echoing back to last year starting to show.

The prices announced by the AHDB saw the weighted average for a 30kg store pig quoted at £61.31, and the weighted average for a 7kg weaner rise by 51p to £43.01.