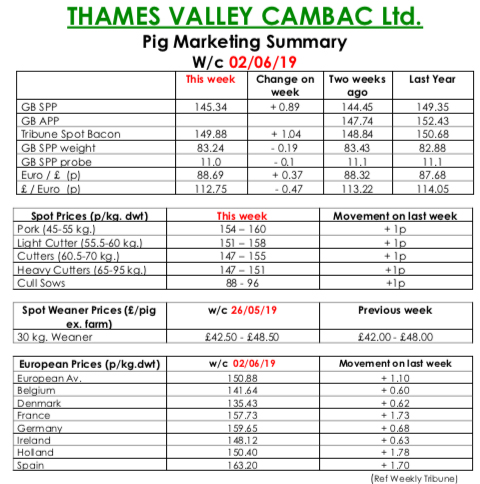

This week’s Slaughter Pig Marketing Summary reported that the change in month saw little change in market sentiment. While supply continued to trend on the tight side, demand from the retail sector in particular was described as uninspiring. The end of month syndrome may be partly to blame, but it caused one or two of the majors to trim kills again.

Prices however, continued to improve, helped by another decent rise in the SPP, and most weekly contract contributions were 1p stronger. Another monthly contribution saw a 5p increase, and this will all feed into other market fundamentals in the coming weeks. The fresh meat market was hoping for a barbeque weekend to kick start some more demand, and prices were generally up 1p to 2p.

The cull sow market saw good demand again and prices were a strong stand on.. In Europe, Ireland, Holland and Spain all improved again, and price quotes in sterling were further enhanced by a stronger Euro that ended the week up 0.37p at 88.69p.

The Weaner Marketing Summary, for week commencing May 26, reported that demand continued to be plagued by slow turnaround of finishing units. Supply improved again, with better production being seen in many cases.

Prices continued to rise however, reflecting the improved nature of the market. The prices announced by the AHDB saw no quote announced for a 30kgs store pig, and the weighted average for a 7kg weaner rise by 43p to £36.65.