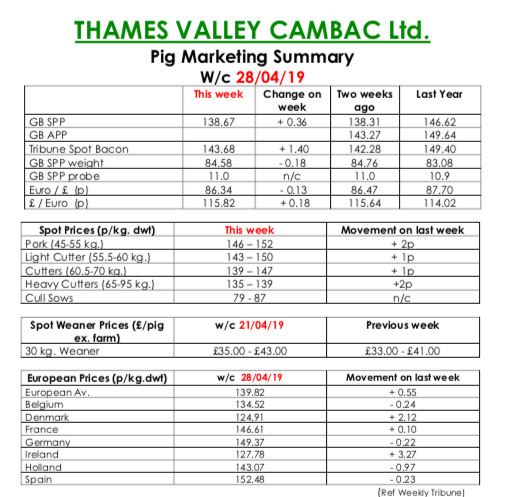

This week’s Pig Marketing Summary from Thames Valley Cambac reported that with a good, warm barbeque Easter behind them, most of the majors looked to replenishing stocks, and the majority planned a full weeks processing. The only difference was that some chose a lighter kill Friday, as this would be cut on the subsequent May Bank Holiday Monday.

Supplies were tighter still, and average weights continued to fall. The good news was that prices improved, with contract price contributions ranging up 2p’s and 3p’s in weekly priced contracts, to a massive teen rise in one monthly priced agreement. This will have the effect of fuelling an upward trend in SPP.

Demand improved in the fresh meat market as well with costly imports driving occasional buyers back to home produced supplies. Prices improved in a range of 1p to 4p. The cull sow market stood on again, as the market got back up to speed after the Easter break. In Europe, Ireland and Denmark played catch up adding four and three euro cents respectively, while the other markets were similar. Price quotes in sterling were tempered however, by a weaker euro that ended the week down 0.13p at 86.34p.

The Weaner Marketing Summary, for week commencing April 21, reported that supplies tightened a touch again with 7kgs weaner numbers steadier, and 30kgs stores remained scarce.

Demand picked up again, and while not buoyant, prices did improve. The prices announced by the AHDB saw no quote given for a 30kgs store pig, and the weighted average for a 7kg weaner fall by 46p to £35.27.