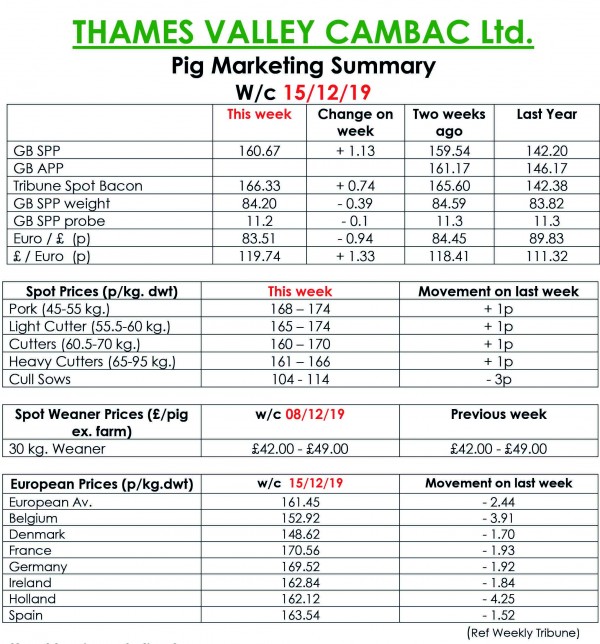

This week’s Slaughter Pig Marketing Summary, from Thames Valley Cambac, reported that, in the last full week of the year, and indeed the decade, most of the major processors had the week planned well in advance.

However, a combination of poor factory reliability and lack of hauliers put paid to some requests for changes. Prices improved again, helped by a stronger SPP which rose 1.13p to 160.67p. Supplies were tighter, and weights continued to trend lower.

The fresh meat market saw good demand in anticipation of Christmas, and prices generally rose 1p to 2p. The election result saw sterling strengthen to a 3.5 year high against the Euro, but this had a detrimental effect on sow prices with most quotes 3p lower.

In Europe, Holland and Belgium reversed the gains of the week before falling 3 and 2.5 euro cents respectively, but all other quotes were similar. However, the much weaker euro had a dramatic effect on quotes in sterling, ending a turbulent week down 0.94p at 83.51p – a level not seen since July 2016.

The Weaner Marketing Summary, for week commencing December 8, reported that supply and demand remained out of synch, with some producers resigned to retaining the batches they had on offer.

The prices announced by the AHDB saw no quote given for a 30kg store pig, and the weighted average for a 7kg weaner rise by 71p to £41.60p.