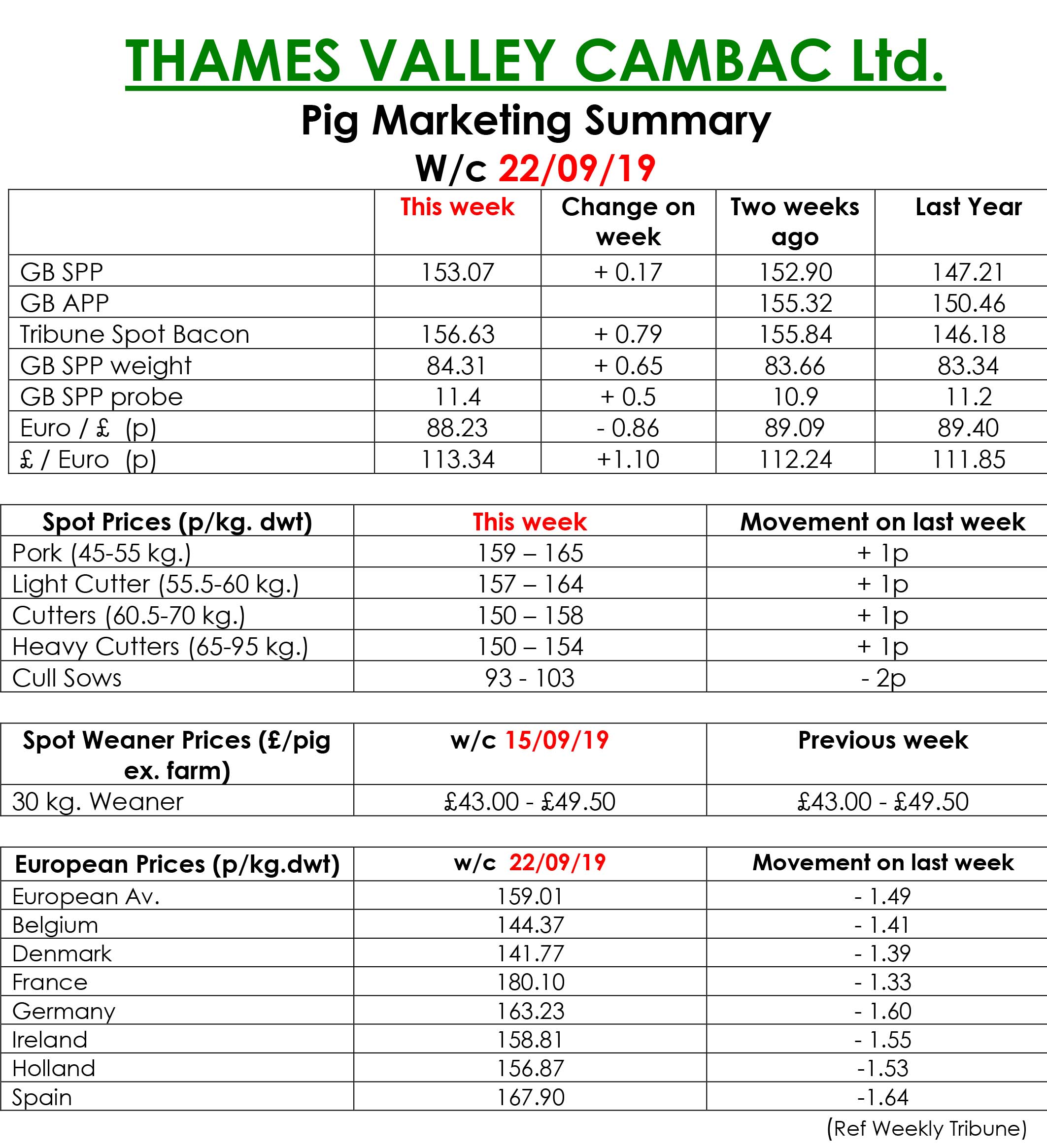

This week’s Pig Marketing Summary, from Thames Valley Cambac, reported that the market is defiantly improving. With all processors that have a weekly input element increasing, the SPP returned to its upward trend, one which we now expect to continue.

Most of the processors are now wanting their full numbers and in some cases extra.

Last week and this week is the monthly negotiations with the majors for their monthly input prices. With pigs in such demand now, these processors can ill afford to be out of line or they will find themselves wanting when it comes to their volume! The only grey cloud was the slight reduction in sow prices which was just a reflection of sterling strengthening from the previous Friday now at 1.134 (88.23p) an improvement from 1.124 (89.09p)

The Weaner Marketing Summary, for week commencing September 15, reported that the weaner and store market was very similar, with the continued shortage of fattening space affecting market sentiment. The prices announced by the AHDB saw the weighted average for a 30kg store pig rise by 78p to £52.87 and the weighted average for a 7kg weaner rise by £1.43 to £40.78p.