This week’s Pig Marketing Summary from Thames Valley Cambac reported that the first full week of the New Year is always a catch-up week, and this year proved no exception.

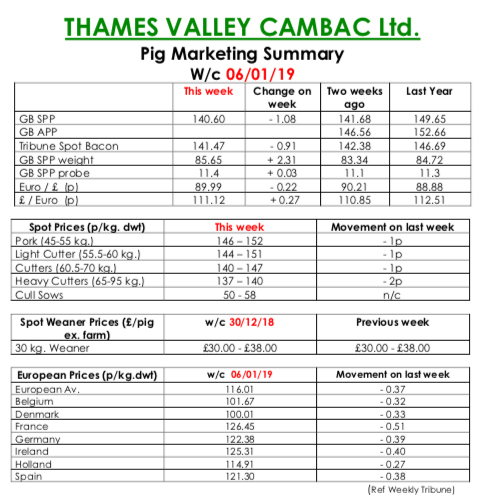

Demand was steady with some processors cutting kills, while others kept to strict contract numbers. There was an improvement in supply from many producers, eating into the backlog caused by Christmas. Contract price contributions eased a penny, and there was a large fall in the SPP. It looks like this fall has been magnified by a small sample size of bigger, fatter pigs, so it will be interesting to see if the SPP announced next week shows a reverse.

The fresh meat market was quieter, with many wholesalers keeping intakes tight, and prices generally eased a penny. The cull sow market saw healthy volumes entered and prices stood on. In Europe, all quoted countries stood on, but prices eased in sterling terms, as the Euro weakened slightly to end the week down 0.22p at 89.99p.

The Weaner Marketing Summary, for week commencing December 30, 2018, reported that demand remained steady with many fatteners worried by increased feed costs impacting on the bottom line. Supply was still tight however, as these are the litters that were conceived in the hot weather last summer.

The prices announced by the AHDB saw the weighted average for 30kgs stores fall £3.07 to £44.54, and the weighted average for a 7kg weaner fall by 82p to £35.62.