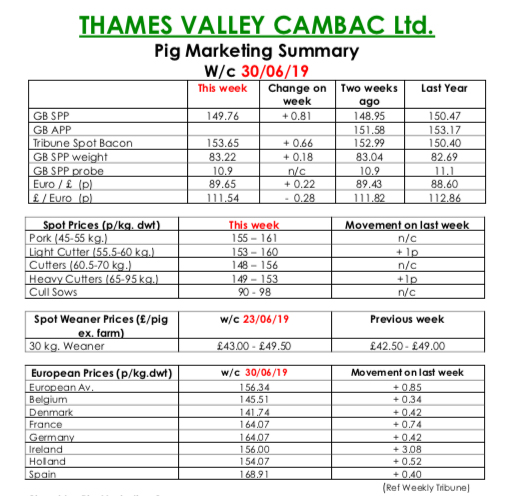

This week’s Pig Marketing Summary, from Thames Valley Cambac, reported that trade continued to struggle with many processors stating that retail demand was still poor.

The much-heralded warmer spell may spark some barbecue interest, but the market needs a major change of direction if we are going to reflect what is happening to continental prices. Demand was lacklustre at best, and kills were cut at more than one of the majors. Contract prices increased however, with some weekly and monthly contributions nicely stronger.

Supplies improved slightly, reflecting the better production conditions in recent times. The fresh meat market was a touch more buoyant with limited import competition helping sales to the high street. The cull sow market stood on again pricewise, with supplies more plentiful than of late.

European prices were generally static, with the exception of Ireland which added three euro cents. Price quotes in sterling were enhanced however, by a stronger euro that ended the week up 0.23p at 89.65p.

The Weaning Marketing Summary, for week commencing June 23, reported that supply continued to improve with 7kgs weaners generally more plentiful. Fatteners struggled, however, to accommodate any batches over and above contracted numbers. The prices announced by the AHDB saw no quote issued for a 30kg store pig and the weighted average for a 7kg weaner fall by 23p to £36.48p.