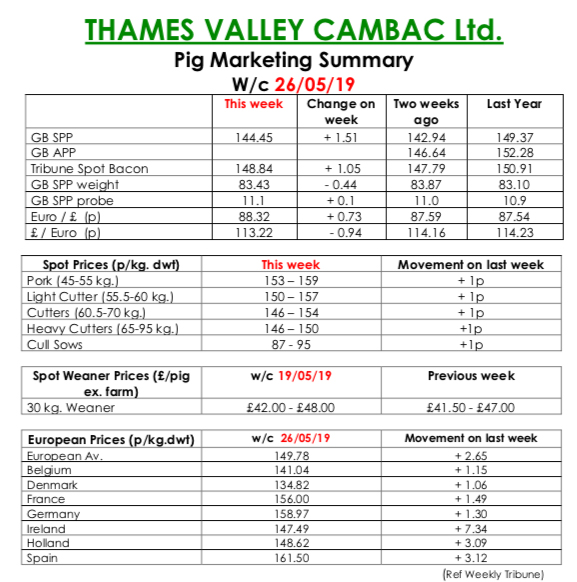

This week’s Slaughter Pig Marketing Summary said that the late May Bank Holiday did not affect any of the majors with all deciding to work a full week. Retail demand was again described as lacklustre by one or two, and numbers were trimmed as a result.

Supply remained tight, and there is little sign of any short term improvement. Prices continued to improve with some monthly contract contributions up as high as 10p, and weekly quotes up 1p.

Coupled with another strong showing by the SPP, it meant that all contract prices saw healthy increases. The fresh meat market continued in a positive vein, with good demand being seen from the high street, and prices were up 1p to 2p as a result. The cull sow market was similar, as exporters had to contend not only with our Bank holiday, but another one in Germany next Thursday. In Europe, Ireland added another seven euro cents, and there were healthy rises in Spain and Holland. Price quotes in sterling were further enhanced by a stronger Euro that ended the week up 0.73p at 88.32p.

The Weaner Marketing Summary, for week commencing May 19, stated that supply improved a touch this week, but met steadier demand due to delayed turnaround of some finishing units. Prices increased in some cases however, as did any contract pigs linked to an appreciating SPP.

The prices announced by the AHDB saw the weighted average for a 30kgs store pig quoted at £47.86, and the weighted average for a 7kg weaner rise by 49p to £36.22.