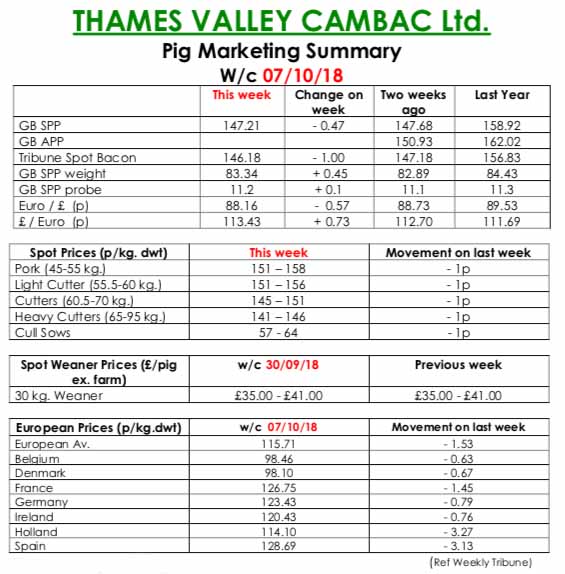

This week’s Slaughter Pig Marketing Summary from Thames Valley Cambac reported on severe breakdowns at multiple processors. Reasons were many and varied, but focussed minds on how vulnerable our end of the supply chain is when a factory cannot accept pig deliveries.

Solutions ranged from hastily arranged Saturday kills to numerous hundreds rolled into this trading week. Supply was a touch higher again, with pigs growing better in the cooler weather. Demand was steady with some majors struggling to take all that was offered. Prices edged downwards, with most weekly price contributions down a penny.

The fresh meat market continues to struggle with reports of keenly priced imports dampening spirits. Cull sow prices eased a penny on the back of currency, and numbers were on the tight side. In Europe, Holland and Spain fell 3 eurocents, but there was some welcome stability from the German market. All quotes in sterling were further eroded by a weaker euro that ended the week down 0.57p at 88.16p.

The Weaner Marketing Summary, for week commencing September 30, reported that the market remained in a very poor state with little demand for any supplies outside contractual arrangements.

Supplies of both 7kg weaners and 30kg stores remained ample, with only any with a Freedom Food ticket being of interest. The prices announced by the AHDB saw the weighted average for a 30kgs pig fall by £3.29 to £51.87 and the weighted average for a 7kg rise by £2.82 to £37.32.