This week’s Pig Marketing Summary from Thames Valley Cambac reported that mediocre demand was a common feature, with some of the majors taking less than their contract commitments. This practice is increasingly common, and sets an uncomfortable precedent for when the market turns.

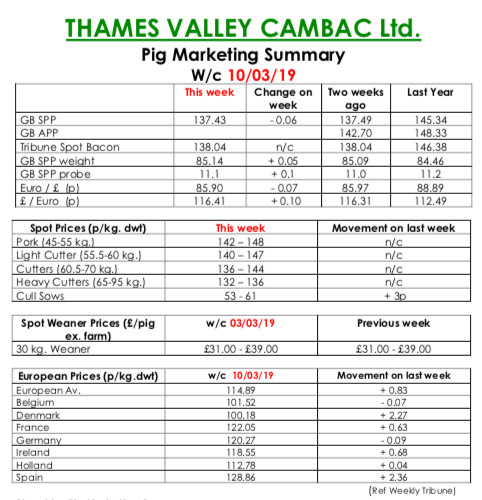

Supply remained manageable, but some weights were stubbornly high. All weekly contract price contributions stood on, but spot bacon trade was minimal. The fresh meat market continued in its poor run, with little spark from any of the wholesalers. The bright spot of the day was reserved for the cull sow market where improved continental trade filtered back to increasing our prices by 3p.

In Europe, Spain continued its price rally adding another 2.9 euro cents, and Demark saw a similar rise. Price quotes in sterling were tempered slightly by a continuing weakness in the euro that ended the week down 0.07p at 85.90p.

The Weaner Marketing Summary, for week commencing March 3, reported that demand improved slightly, and was matched by better supply from numerous sources. This gives credence to the reports of slightly better weaning’s recently.

The prices announced by the AHDB saw no quote given for a 30kgs store pig, and the weighted average for a 7kg weaner fall by £1.38 to £35.39.